Fixed Indexed Annuities and Variable Annuities – How do they compare?

More often than not Variable Annuities are purchased based on three key features:

- A Withdrawal Benefit Rider

- A Death Benefit Rider

- Upside Potential

Do Variable Annuities have a place in retirement planning? Yes and no. If we look at their Withdrawal Benefit Riders that are similar to the Income Riders found on most Fixed Indexed Annuities, how do they compare? In most cases Fixed Indexed Annuities offer higher Income Value growth (as high as 8% compounded), longer deferral periods before income is started and higher payout percentages when income is actually started. Based on numerous surveys, the main concern for most retirees is outliving their retirement savings. While both types of Annuities offer income benefits, ultimately it’s how much income that is actually paid out that is most important. More often than not, the Fixed Indexed Annuity will pay more in income than a Variable Annuity.

What about a Death Benefit Rider? Both Variable Annuities and many Fixed Indexed Annuities offer a death benefit that is greater than the actual Contract Value of the annuity. For many clients, what good does it do to have a high death benefit, an income rider that pays out an average income and a potentially diminishing contract value due to market volatility? I suppose it’s nice for their beneficiaries, but it doesn’t do a whole lot of good if the client’s main goal is to preserve principal and not outlive their retirement savings.

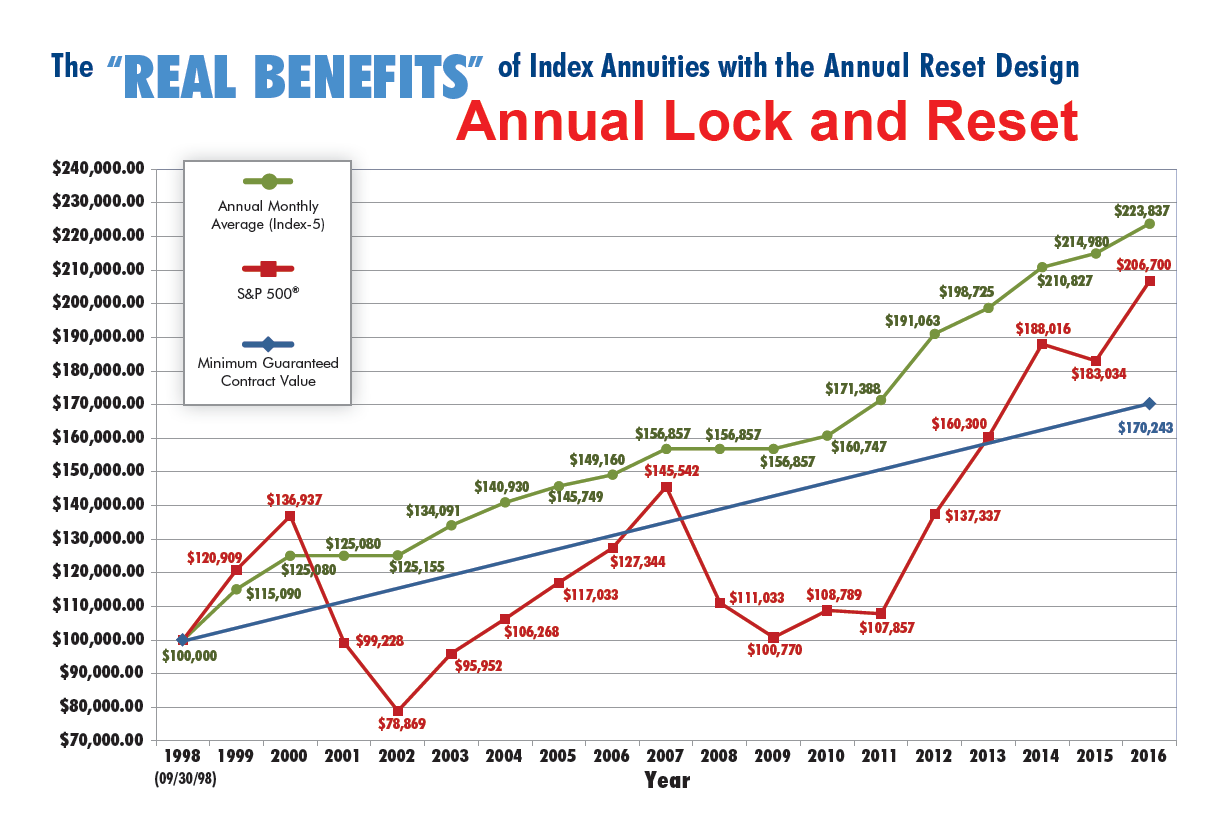

Can a Variable Annuity provide upside potential? Absolutely. But therein also lies the problem. Due to market volatility, a Variable Annuity can also take away much of a person’s life savings in a very short amount of time.

Let’s take a scenario where someone puts $100,000 into a Variable Annuity and two years later, has only $50,000 in the Contract Value, but has $120,000 of Death Benefit and Income Value. What will the advisor who sold the Variable Annuity tell the client? Don’t worry. Even if the market doesn’t recover, you’re okay. You’ll still be able to get all the income you need for the rest of your life, and you also have a large death benefit for your beneficiaries. Well if that’s the case, why in the world would you purchase the Variable Annuity to begin with? If the income and death benefit are the overriding concerns, why risk losing much of your money when you don’t have to?

With a Fixed Indexed Annuity, you have an Income Rider that in most cases is better than the one in the Variable Annuity, a Death Benefit Rider that is comparable to the ones found in the Variable Annuities and best of all, the client never has to put their money at risk! And let’s not forget that the Fixed Indexed Annuities even in today’s low interest rate environment still have the power to outperform the Variable Annuity over a period of time.

Oh, and one more thing. Don’t forget about the fees. The Fixed Indexed Annuity products from the Statewide Retirement Planning Co. carriers have Income Riders with costs that range from 0% up to .95% and combined with a Death Benefit Rider can be as much as 1.15%. That’s it! There are no other fees with Fixed Indexed Annuities. In fact, if the client doesn’t care about income or death benefit, they can have zero fees associated with their annuity. With Variable Annuities, there can be a fee for the Income Rider, a fee for the Death Benefit rider, a Mortality and Expense Fee, an Administrative Fee and Subaccount Fund Fees. It’s not uncommon for the average Variable Annuity to have anywhere between 4 and 6% in fees.

Comparison between Variable Annuities and Fixed Indexed Annuities

|

Fixed Indexed Annuities |

Variable |

|

|

Withdrawal Benefit Rider |

||

| Income Value Growth |

Higher |

Lower |

| Deferral periods |

Longer |

Shorter |

| Payout Percentage |

Higher |

Lower |

| Amount of Income payout |

Higher |

Lower |

|

Account Value |

Guaranteed never to lose principle due to market performance | Risky – Varies up and down with market volatility and is greatly affected by fees. |

|

Death Benefit Rider |

Not very relevant if the main purpose is to preserve principle and provide retirement income. | |

|

Fees |

0 fees unless voluntary options are selected e.g. lifetime income rider and/or death benefit rider. Max approx 1.25%. | Typically 4% to 6%

* See Below for Details |

*Typical Fees in Variable Annuities:

| Administration Fees | .25% – .5%/yr |

| Mortality Expense Fee | 1% – 2%/yr |

| Mutual Fund Fees | .5% – 2.5%/yr |

| Income Rider Fee | .6% – 2%/yr |

| Death Benefit Fees | 1% – 2%/yr |

| Total | 3.4% – 9% |

| Average | 4% – 6% |